Struggling with a mountain of credit card debt? PayOff offers a smarter,

faster way to clear your dues and reclaim your financial freedom.

Curious about savings and a debt-free life? Input your credit card balance to see PayOff’s magic—lower rates, one easy EMI, fast results.

Debt-Free by Aug 2027* or sooner

At PayOff, we simplify debt consolidation so you can focus on what matters—living debt-free.

Share your credit card debt details in a few easy steps.

Replace multiple payments with a single, affordable monthly EMI.

We work with our trusted lending partners to create a low-interest loan tailored for you.

Save on interest and clear your debt faster than ever.

Use the loan to pay off your high-interest credit card balances.

Getting out is easier than you think. Round up these basics, and we’ll take it from there:

PAN Card

Aadhar Card

Address Proof (e.g., utility bill, rental agreement)

Recent Credit Card Statements

Salary Slips (if salaried) or ITR (if self-employed)

Bank Account Statement (last 3 months)

PAN Card

Aadhar Card

Address Proof (e.g., utility bill, rental agreement)

Recent Credit Card Statements

Salary Slips (if salaried) or ITR (if self-employed)

Bank Account Statement (last 3 months)

Real stories from folks who were stuck—just like you—and found relief with PayOff. No more panic, no more burden.

I was stuck paying just the minimum due on three credit cards. Every month it felt like I was running in circles. Through Payoff, I finally got a single loan with a much lower interest rate. Now I know exactly what I owe and when it will end. Honestl...

As a freelancer, my income is up and down. Managing 4 different EMIs was a nightmare. Payoff helped me combine everything into one loan with a EMI. Felt like someone was finally on my side.....

My CIBIL had taken a hit because of delayed payments. I didn’t think anyone would give me a loan. But Payoff didn’t reject me outright — they guided me on how to qualify and offered a plan that suited my salary. It’s a relief to be rebuilding...

We had wedding expenses, a personal loan, and credit card bills piling up. Payoff helped us combine it all. Now instead of three EMI dates and confusion, we have one EMI and a fixed end date. It’s helped us plan better as a couple.....

I was paying high interest for 5 years and still the loan balance was not going down. Through Payoff, I understood how consolidation works. They helped me close old debts directly and now I have one EMI with clear terms. Wish I had done this earlier....

Got doubts? We’ve got answers. Here are the most common questions about PayOff:

Debt consolidation combines multiple debts—like credit card balances—into one loan with a lower interest rate. For example, if you owe ₹4,15,000 on one card at 20% interest and ₹2,49,000 on another at 18%, PayOff can help you consolidate them into a single ₹6,64,000 loan at 10%. This saves you money on interest and simplifies payments, helping you clear debt faster than just paying minimums. With PayOff, you get a tailored solution to manage and eliminate your credit card debt efficiently.

Paying credit cards directly often means high interest rates (24-40% in India) and minimum payments that barely reduce your balance. Debt consolidation replaces those with a single loan at a lower rate (e.g., 10-15%), so more of your payment goes toward the principal. It’s like fixing a leaking pipe—your money stops draining into interest, helping you pay off debt faster.

You don’t necessarily need a good credit score to apply for a PayOff debt consolidation loan, but your credit score will impact your eligibility and the terms you’re offered. PayOff works with a range of credit profiles, and while a higher score (typically 670 or above) can secure lower interest rates, they may still have options for those with fair or lower scores. Factors like your income, debt-to-income ratio, and repayment history also play a role in approval. To find out exactly where you stand, you can check your eligibility with PayOff—often with no impact to your credit score—allowing you to explore personalized solutions regardless of your credit situation.

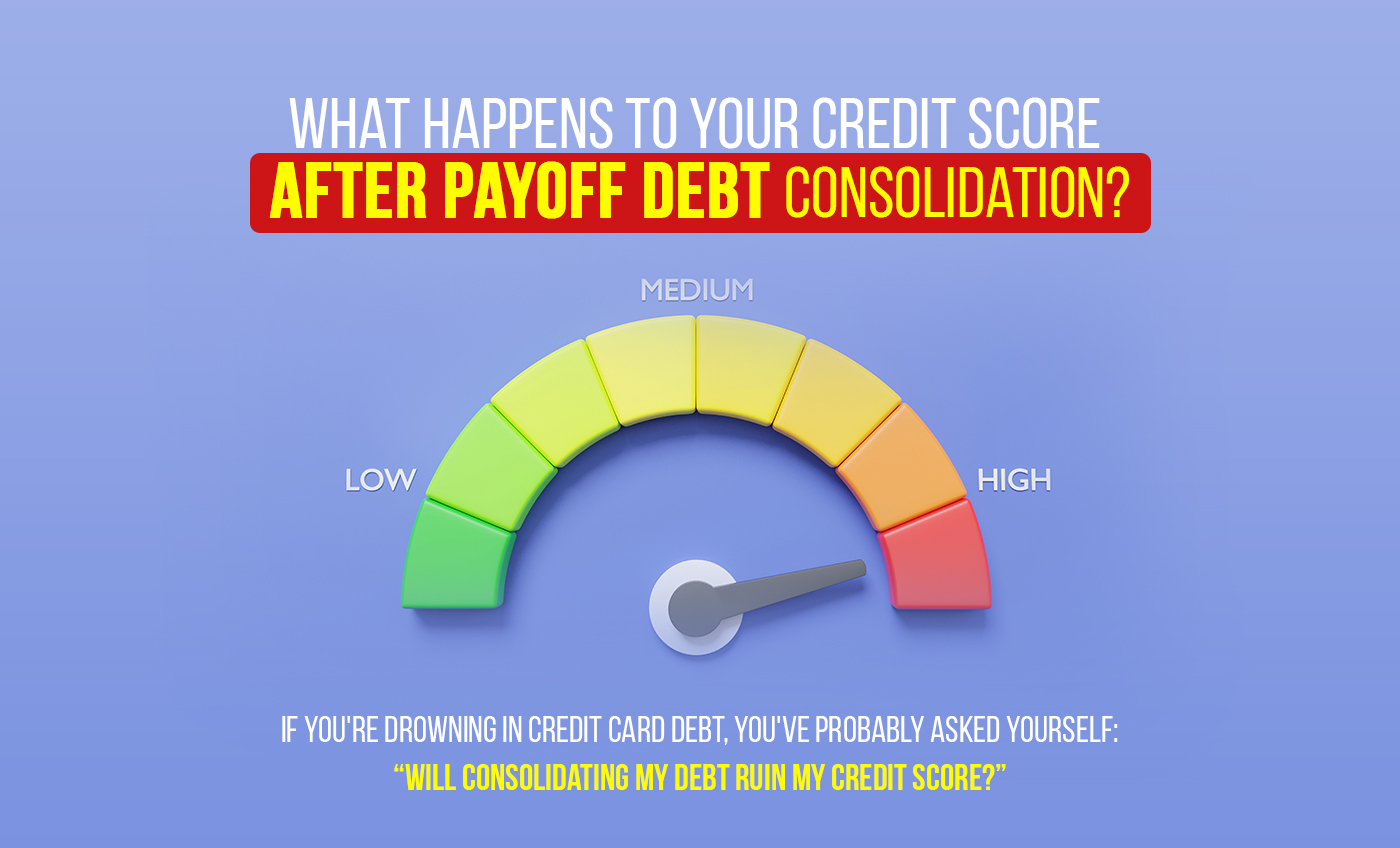

Consolidating your debt with PayOff can affect your credit score in both the short term and long term, depending on how you manage the process. Initially, applying for a PayOff debt consolidation loan may cause a small, temporary dip in your score due to a hard inquiry when PayOff checks your credit. This typically drops your score by a few points, but it usually recovers within a few months. On the positive side, using PayOff to consolidate high-interest credit card debt can lower your credit utilization ratio—how much of your available credit you’re using—which often boosts your score over time, as long as you don’t rack up new debt. Plus, making on-time payments on your PayOff loan can strengthen your payment history, the biggest factor in your credit score. However, if you miss payments or close old credit accounts after consolidating, it could hurt your score by shortening your credit history or reducing available credit. Overall, consolidating with PayOff is likely to help your credit in the long run if you manage it responsibly.

How much you save by consolidating your credit card debt with PayOff depends on the rates and terms you qualify for. For example, if you have ₹8,30,000 in credit card debt at 22% interest and pay ₹20,750 monthly, it could take over 8 years to clear, with ₹9,13,000 paid in interest alone. By consolidating with PayOff at a lower rate—say, 10%—you could pay it off in just 4 years, with only ₹1,66,000 in interest. That’s a savings of ₹7,47,000. With PayOff, your exact savings will hinge on your personalized loan offer, but the potential to cut both time and interest is significant.

The interest rates for PayOff’s debt consolidation loans vary depending on factors like your credit score, loan amount, and repayment term. Typically, PayOff offers rates ranging from around 6% to 20% APR, aligning with common rates for debt consolidation loans. If you have excellent credit (say, a score of 720 or higher), you might qualify for a lower rate closer to 6%-10%, while those with fair or lower credit (below 650) could see rates closer to 15%-20%. To get an exact rate tailored to your situation, you can check your eligibility on the PayOff website—often with a pre-qualification option that won’t affect your credit score. This way, PayOff can provide a personalized quote based on your financial profile.

Yes, you can consolidate debt from multiple credit cards into one plan with PayOff. Whether you’re juggling balances across two, three, or more cards, PayOff allows you to combine them into a single loan with one monthly payment. For instance, if you have ₹2,00,000 on one card, ₹1,00,000 on another, and ₹80,000 on a third, PayOff can roll them into a single ₹3,80,000 loan, often at a lower interest rate than your cards’ average APR. This simplifies your finances and could save you money on interest, making it easier to pay off your debt faster with PayOff’s streamlined plan.

PayOff makes debt consolidation simple by connecting you with our trusted lending partners. You start by submitting an online application with details about your debts, income, and financial situation. PayOff evaluates your profile and matches you with a suitable loan offers from our network. For example, if you have ₹6,00,000 in credit card debt, a lending partner might offer a loan at 12% interest. Once you accept the terms, the lender pays off your creditors directly, consolidating your debts into one loan with a single monthly payment. You then repay the lender over a fixed term, usually 2-5 years, with payments tailored to your budget.

Explore expert insights and tips from our team to help you take charge of your finances.

If you’re like millions of Indians, you’ve pro...

PayOff

If you’ve ever felt the crushing weight of credi...

PayOff

“It started with one swipe. Then another. Before...

PayOff

You shouldn’t have to choose between paying your...

PayOff

PayOff

DigitMoney Technologies Pvt Ltd.